[INBOX] My insurance has fought me for every procedure, ER visit and doctor bill I have incurred. #ObamaCareHurts #WhatsYourStory? Email it to us at mystory@brokenobamacarepromises.com

Posted by Broken ObamaCare Promises on Monday, January 30, 2017

News

The Right Prescription: Obamacare Is Killing Rural Hospitals and Their Patients

David Catron | January 9, 2017, 12:04 AM

Since 2010, rural hospitals have been put out of business at a rate of one a month.

Among the talking points deployed by Obamacare apologists in their effort to save “reform” is the claim that repeal will cause thousands to die due to the loss of health insurance. This nonsense is based on the fiction that repeal will cause tens of millions to instantly lose health coverage and on debunked studies showing that the lack of insurance causes premature death. Strangely, the compassionate champions of the potentially uninsured seem unmoved by the very real carnage wrought by Obamacare’s destruction of rural hospitals. Since 2010, 80 such facilities have closed, a trend that is killing patients right now.

Most of these shuttered hospitals provided the only realistic source of accessible emergency care for patients living in the rural communities they served. If you live in the area once served by Colusa Regional Medical Center in rural California, for example, you would be ill-advised to have a heart attack. To get you to a hospital your ambulance will have to drive past that now-closed facility in order to get you to the nearest ER. When asked why the hospital was forced to close, the CEO included the following among the principal reasons: “The Affordable Care Act and its reimbursement model for Medicaid and Medicare.”

This model is the result of a bait-and-switch perpetrated on the hospital industry by the White House and congressional Democrats. In 2009, the industry agreed to support Obamacare by accepting $155 billion in cuts to their Medicaid and Medicare payments in exchange for a promise that “reform” would flood hospitals with millions of newly insured patients whose coverage would offset the concession. Predictably, Obamacare fell short of its goals and 97 percent of its enrollees were dumped into Medicaid, which pays hospitals well below the cost (cost, not charges) of treating patients covered by that program.

All of this means that rural hospitals are rapidly becoming extinct and that, if you are one of the 60 million Americans who make their homes in rural areas, this is a very dangerous trend for your health. In other words, when your ambulance has to be driven past a facility that has been forced out of business by Obamacare, your chances of dying on the way to — or after you finally reach — the next hospital down the road have been significantly increased. Unlike the “research” predicting zillions of deaths if the law is repealed, this is the conclusion of a legitimate study reported by the American College of Emergency Physicians:

Patients admitted to the hospital in the geographic vicinity of other emergency department closures had 5 percent higher odds of inpatient mortality than patients who were admitted in areas where no emergency department had closed.… Odds of mortality increased by 10 percent for non-elderly adults, by 15 percent for patients with AMI, by 10 percent for patients with stroke and by 8 percent for patients with sepsis.

Nonprofit Quarterly reports that 673 rural hospitals are vulnerable to closure. In other words, their financial situations are comparable to those which have closed their doors since 2010. And now, in addition to being underpaid by Medicaid, they are of course suffering from yet another problem directly attributable to Obamacare: “Increasing insurance deductibles and co-pays are leaving insured patients and their families with larger medical bills.… Some families are unable to make timely payment, adding to hospitals’ cash flow problems.” And it gets worse. NPQ also reports another destructive proposal by the Obama administration:

A looming threat for rural hospitals… is a proposal by the Inspector General (OIG) of the U.S. Department of Health and Human Services (HHS) to reduce rural hospitals’ reimbursement for so-called “swing bed” reimbursement by up to 462 percent. Swing beds are beds recognized by Medicare as being available for use either as an acute hospital bed or as a rehabilitation bed (usually post-surgery but before a patient is cleared to return home).

If the geniuses who run the Obama administration’s health care bureaucracies were deliberately attempting to destroy the rural hospital system, they couldn’t do much more damage. Rural facilities constitute about 37 percent of America’s community hospitals. If they continue to go under at the rate they have been failing since Obamacare reared its ugly head, patient access will plummet precipitously, hundreds of thousands of hospital and hospital related community jobs will disappear, and hundreds of billions will vanish from the nation’s Gross Domestic Product. And, of course, a lot of people living in America’s heartland will die.

Obamacare apologists predict all manner of dire consequences if the widely reviled law is repealed, including thousands of unnecessary patient deaths. But they have ignored the rural health crisis that was caused by the “reform” law and is killing people right now. This is just one more reason to ignore the law’s dead-enders and repeal this travesty now.

Premium Increase and High Deductibles!

52% increase. $1100/month and have to pay 100% of medical costs until I reach out of pocket. @BrokenObamaCare pic.twitter.com/avGNQdafLT

— Amanda Hanna (@Adea03Hanna) January 6, 2017

Obamacare Plans Don’t Always Include Top Cancer Centers

Being told that you have cancer can be scary. Discovering that your health insurance plan doesn’t give you access to leading cancer centers may make the diagnosis even more daunting.

As insurers in the plans set up under the Affordable Care Act shrink their provider networks and slash the number of plans that offer out-of-network coverage, some consumers are learning that their treatment options can be limited.

One reader wrote to Kaiser Health News last month saying that she was dismayed to learn that none of the plans offered on the New York health insurance marketplace provides access to Memorial Sloan Kettering Cancer Center in New York City, where she is a patient.

Memorial Sloan Kettering is a well-regarded cancer center that is affiliated with two key organizations: the National Comprehensive Cancer Network and the National Cancer Institute. The cancer center participates in New York’s Essential Plan, which is available to lower income people on the state’s exchange, but doesn’t participate in any of the regular plans designated as bronze, silver, gold or platinum.

The National Comprehensive Cancer Network is an alliance of 27 cancer centers. Member physicians and researchers develop widely recognized clinical practice guidelines.

The National Cancer Institute recognizes many cancer centers for their scientific leadership and research. The 69 NCI-designated cancer centers can offer patients access to cutting-edge treatments and clinical trials. All 27 NCCN centers are also designated by the NCI.

It’s unclear the extent to which these cancer centers, which are often but not always affiliated with large academic institutions, are included in the provider networks of marketplace plans nationwide. A survey by Avalere Health in 2015 found that three-quarters of NCI-designated cancer centers said they participated in at least some exchange plans, and 13 percent said they were included in all exchange plans in their state. However, of the 25 percent of centers that didn’t participate in any exchanges, many were in states with large numbers of exchange enrollees, including Texas and New York, the survey reported.

Does it matter if someone with a cancer diagnosis gets treatment at one of these centers rather than at a community hospital or some other site? Research suggests that it may. A study found that adult patients between the ages of 22 and 65 who were newly diagnosed with one of several types of cancer — breast, colorectal, lung, pancreatic, gastric or bile duct — were 20 percent to 50 percent more likely to die from the disease if they were initially treated at a place other than an NCI-designated comprehensive cancer center.

The study, which analyzed the five-year survival rates of nearly 70,000 patients whose cancers were reported in the Los Angeles County cancer registry between 1998 and 2008, was published in the journal Cancer in 2015.

Researchers hypothesize that the cancer centers’ multidisciplinary approach to decision-making, supportive care and access to cutting-edge treatment, among other things, contribute to the superior outcomes at comprehensive cancer centers, said Dr. Julie Wolfson, a pediatric oncologist at the Institute for Cancer Outcomes and Survivorship at the University of Alabama at Birmingham who was a co-author of the study.

“The goal is to find out what is different about these places and then disseminate that to other” treatment sites, Wolfson said.

Often there are factors aside from survival rates that contribute to a patient’s decision about where to go for care, said Dr. Robert Carlson, CEO of the National Comprehensive Cancer Network. Those factors can include support systems that patients already have in place and concerns about nonmedical costs, such as housing and transportation.

“Most patients, if offered the option to go to a major cancer center — especially if it involves traveling — will decline it,” Carlson said.

Some cancer centers aim to give patients access to both types of facilities. City of Hope cancer center’s main academic campus is in Duarte, Calif., in Los Angeles County. That’s the best site for patients when their cancers are rare or advanced, optimal treatment isn’t clear or they could participate in a clinical trial, said Dr. Harlan Levine, the chief executive of the City of Hope Medical Foundation. But the cancer center also owns a network of 14 community cancer clinics located in Southern California for patients who can be effectively treated in that setting, he said.

City of Hope participates in two plans that are offered on California’s exchange, Blue Shield and Anthem, and its physicians are in-network for the exchange’s Oscar health plan. But most people don’t check access to cancer care when they shop for a plan. “Cancer is an infrequent purchase from a marketing point of view,” Levine said. In many cases, patients don’t realize their lack of access until after their diagnosis, when it may be too late.

Cancer centers may try to work with patients to enable their treatment.

“We understand that each patient has a unique financial situation and we work with our patients, especially those in active treatment, to ensure they receive the care needed and that their treatment is uninterrupted,” said Ruth Landé, senior vice president for patient care revenue at Memorial Sloan Kettering. “We have patient financial services representatives available to assist patients who do not have health insurance or whose insurance may not cover all charges.”

Patients who believe that it’s critical to be treated at a cancer center that’s not in their insurance network do have some recourse.

When people receive a cancer diagnosis, it’s “overwhelming,” said Anna Howard, a principal for policy development at the American Cancer Society’s Cancer Action Network. “You may not be aware of the fact that if your insurance plan says you don’t have coverage at a cancer center you can file an appeal.”

Appealing the insurer’s decision doesn’t guarantee success, however.

“Anecdotally,” Howard said, “we hear that it depends on the specific individual and type of cancer.”

Kaiser Health News is an editorially independent news service that is part of the nonpartisan Henry J. Kaiser Family Foundation. Michelle Andrews is on Twitter: @mandrews110.

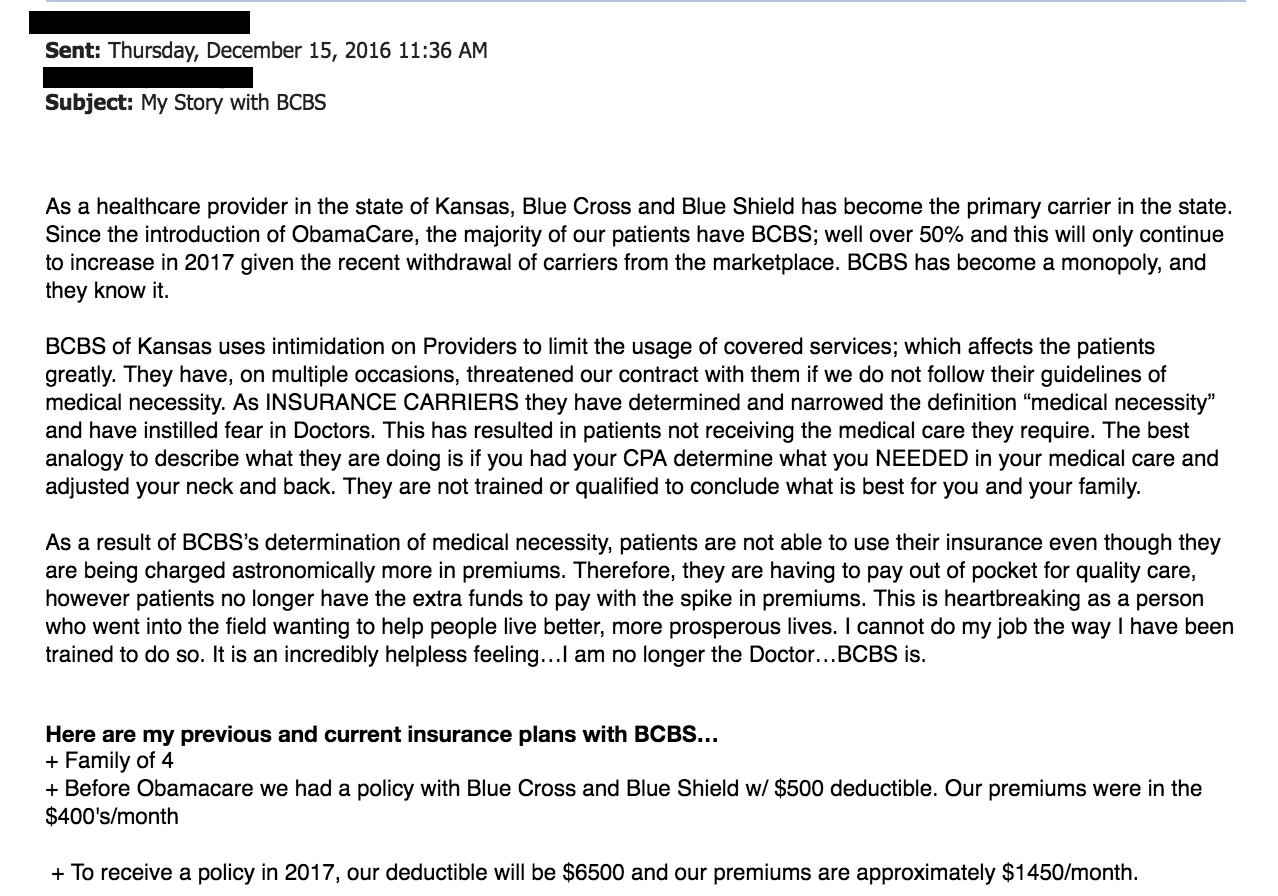

My Story with BCBS

Meet 2 Hurting Americans Who Are Ready for Congress to Repeal Obamacare

Melissa Quinn /

On the night of the election three weeks ago, Rochelle Bird stayed up late watching the returns with a friend.

Bird, a financial adviser from Overland Park, Kansas, recalled being in knots in the days leading up to the election.

“If it didn’t go the way of [Donald] Trump, the next four years and possibly eight were going to be hell on wheels to financially endure in this country,” Bird told The Daily Signal.

So when the Associated Press eventually announced real estate mogul Donald Trump as the winner, Bird let out a sigh of relief.

Public policy affects Bird, as it does many other Americans, and she says she hopes that policymakers will consider people like her while making decisions in Washington, D.C.

Bird doesn’t expect to like everything Trump does after he takes office Jan. 20, but there’s one issue in particular she’s watching: health care.

Bird is one of roughly 10 million Americans who doesn’t receive insurance from an employer—she’s self-employed—and also doesn’t qualify for a subsidy. So when insurers announced double-digit premium increases for 2017, she prepared to pay full price for coverage purchased in the individual market.

And that wasn’t it.

Coventry Health Care sent Bird a notice last month saying it would cancel her policy at the end of the year.

On the first day of open enrollment, the Overland Park resident selected a new plan through Blue Cross Blue Shield of Kansas City, one that is only $50 more than her old policy.

But though Bird’s premiums increased minimally compared to others across the country, her deductible is higher and she has less coverage than with her previous plan.

“I’m paying more for less,” she said.

According to the Obama administration, 20 million Americans gained health insurance coverage under Obamacare. While many of those 20 million may be worrying about the future of their health insurance in a Trump administration, Bird isn’t one of them.

And she’s not alone.

“For the percentage of people who have been helped, it’s significantly impacted people in a disproportionate way,” Bird said of Obamacare. “It’s irrational. If you want to say we want to be a country that makes sure everyone has an option for health care, OK. But we’ve proven this isn’t working.”

Repeal Before Replace

Republicans in Congress voted more than 60 times to repeal the Affordable Care Act, popularly known as Obamacare, and each bill failed to make it out of the Senate and go to the White House.

But following Trump’s victory Nov. 8, GOP lawmakers are fine-tuning their strategy to get a bill repealing the health care law to Trump’s desk in the White House—a bill he is likely to sign.

Trump said repeatedly on the campaign trail he would repeal Obamacare and is in favor of allowing insurers to sell policies across state lines, expanding access to health savings accounts, and creating block grants for Medicaid.

Earlier this month, leaders of the House and Senate budget committees endorsed a repeal plan that involves passing two budget resolutions—one for 2017 and one for 2018—that include instructions for reconciliation, a budget tool that allows legislation to pass the Senate with only 51 votes.

Congressional Republicans used reconciliation to repeal Obamacare in 2015, but President Barack Obama ultimately vetoed the bill earlier this year. Now, they’re looking to use that legislation as a model to roll back the health care law in 2017.

Republicans haven’t yet agreed on a replacement plan for Obamacare, but House Majority Leader Kevin McCarthy, R-Calif., told reporters Tuesday that replacement would come later.

“My personal belief, and nothing’s been decided yet,” McCarthy said, “but I would move through and repeal and then go to work on replacing.”

Republicans have said they want to ensure those with coverage through Obamacare have a smooth transition to the new system, and legislation dismantling the law likely would include a delayed enactment date, giving lawmakers time to craft and pass a new plan.

But some health policy experts believe any Obamacare replacement could take years to put into place.

“If we’ve learned anything, it’s that implementation isn’t automatic,” Timothy Jost, a law professor at Washington and Lee University School of Law, told The Daily Signal.

“The idea that we can repeal by Jan. 6—there are going to be millions grievously hurt by this, including people who have coverage through the Affordable Care Act and don’t have the money and can’t get the money to cover cost-sharing or insurance on their own,” Jost said.

Indeed, some Americans are worried about the future of their coverage come 2018.

In an interview with CNN earlier this month, Ron Pollack, executive director of the pro-Obamacare group Families USA, said there could be significant backlash from consumers if health insurance under Obamacare is taken away.

“There are a lot of things we don’t know yet [about a replacement plan], but we do know there are tens upon tens of millions of people who depend upon the Affordable Care Act, who depend on Medicaid, and, of course, they are terribly worried that the coverage they have would be taken away,” he said.

Still, health policy experts advocating Obamacare’s repeal are encouraging policymakers to set a timeline to ensure reforms are in place by 2019.

In a paper released last week, Nina Owcharenko and Ed Haislmaier of The Heritage Foundation said Congress should not allow provisions of the Affordable Care Act, such as the subsidies, to expire before new measures take effect:

Timing and sequencing of these efforts are complex, and proper execution is critical. Congress, the new administration, and the states should work together to ensure a smooth transition for the repeal of Obamacare and to create a path toward a more patient-centered, market-based approach to reforming the health care system.

‘Cautious Optimism’

Like Bird, Warren Jones, a veterinarian in Missouri, is also optimistic about Obamacare’s repeal and what will replace the law.

“It’s a good thing overall, and I think everybody is open to the optimism of it,” Jones told The Daily Signal. “The media has been portraying it in such a way that Trump was going to take all the insurance away from the people that were insured on Obamacare.”

“He’s not talking about ripping everyone’s insurance away,” Jones said. “He’s talking about replacing it with something better, and that doesn’t mean you take everyone’s insurance away first and let them suffer from that.”

Jones, who also spoke about Obamacare with The Daily Signal last month, has a plan through Blue Cross Blue Shield of Kansas City. The company sent Jones a letter in October notifying him that his monthly premiums would increase from $491 to $716 for 2017.

Jones toyed with the idea of changing carriers, but when rates for Missouri were released before the start of the 2017 open enrollment period, the veterinarian learned that his plan would be the cheapest option available.

As a business owner, Jones said he’s looking forward to the impact that repeal of the health care law will have not only on his own wallet, but also on the business community.

Before, many business owners opted to lessen workers’ hours to below 30 hours per week to avoid having to provide them with health insurance coverage. Jones said he also knows of many employees who were forced to watch their hours and income so they wouldn’t lose their subsidy.

But now that Obamacare is likely to be repealed, he sees “cautious optimism” from his fellow business owners:

They’re going to loosen the purse strings a little to make the repairs and make the growth moves that they want to do to improve their business. People have been holding off to see what direction things were going. Now they know what direction it’s going to go.

There are aspects of Obamacare that Jones would like to see included in a replacement plan, such as the measure that allows those under age 26 to remain on their parents’ plan, as well as the provision that prohibits insurers from discriminating against consumers with pre-existing conditions.

But he said he hopes that any new plan would create high-risk pools, expand access to health savings accounts, and do away with the essential health benefits package, a list of mandatory benefits each plan must cover.

“We might be able to have a choice that makes an affordable plan for us, instead of having to take the one-size-fits-all,” Jones said.

Trump hasn’t yet said whether he plans to roll back any of the regulations implemented as part of Obamacare, but Jones said he hopes the new president takes a more piecemeal approach to changing the law, one that would help eliminate some fear among consumers.

“I understand there are people afraid and worried about it now that they have insurance,” he said, “but I don’t think you’re going to run into a heartless decision that jerks insurance away from people.”

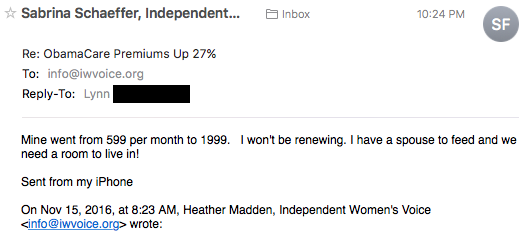

Her ObamaCare Premium Is Over $1,000 Per Month!

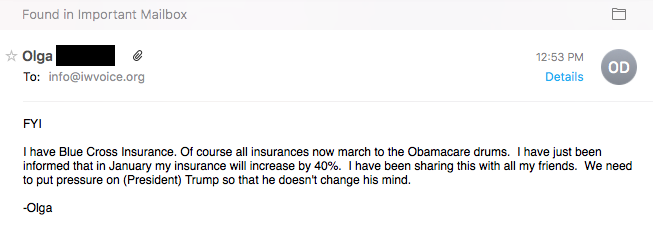

Her Blue Cross Insurance Will Increase by 40% under ACA

A Farmer from Missouri Is Paying Close to $10,000 a Year for Health Insurance and Medication

“That’s what’s happening to Darvin Bentlage, a farmer in southwest Missouri, outside the town of Lamar. Like many farmers, he has been having a rough time recently. He raises corn, soybeans and beef, and prices for all his products have plummeted in the past two years. In late October he was pretty upset because he got a letter from his insurer, Anthem Blue Cross and Blue Shield, saying his policy was going up about $200 a month. Even after his subsidy, he thought he’d be paying $500 a month just for his premium. On top of that he spends about $300 a month on medications to control his diabetes. “So I’m going to be paying close to $10,000 on my medicine and my insurance on a $20,000 income,” he said.”